")

")

")

")

")

")

")

")

")

")

")

")

")

")

Review of the META company and is it really so dangerous to fall by 15% after the report for the 1st quarter of 2024?

![]()

Meta (META) shares fell 15% following its fiscal 1Q24 earnings report.

The main reasons for the stock's decline are that Meta said it expects second-quarter revenue to be between $36.5 billion and $39 billion; the midpoint of the range fell slightly short of the consensus forecast of $38.2 billion. This year, Meta forecasts capital expenditures of $35 billion to $40 billion, up from the previous range of $30 billion to $37 billion - this is due to increased costs associated with with artificial intelligence.

I'd like to remind you that META is up more than 5x from its 2022 lows and may need a break. The market has already rewarded management's actions in a post-ATT world¹.

Anti-Apple

It's no secret that Meta and Apple have ongoing disagreements over opposing views on the future of the Internet.

Apple is known for its closed iOS ecosystem, reluctance to announce artificial intelligence products until they are ready for prime time, and carefully crafted product announcements.

Zuck's scenario looks exactly the opposite:

🔓 Closed or Open: The recent announcements of Horizon OS and Llama 3 make this a classic battle between closed systems like Apple and open models like the ones that won the PC era.

🧪 Testing and Iteration: Using Meta AI, Zuck uses his Reels playbook: launch small, refine, scale, and monetize later.

🤳Random Announcements: Zuck presented important company initiatives with a relaxed atmosphere as a content creator.

1. Meta-first quarter of FY24

Let us remind you that Meta has two business segments:

- FoA: family of applications (Facebook, Instagram, Messenger and WhatsApp).

- RL: Reality Labs (virtual reality hardware and supporting software).

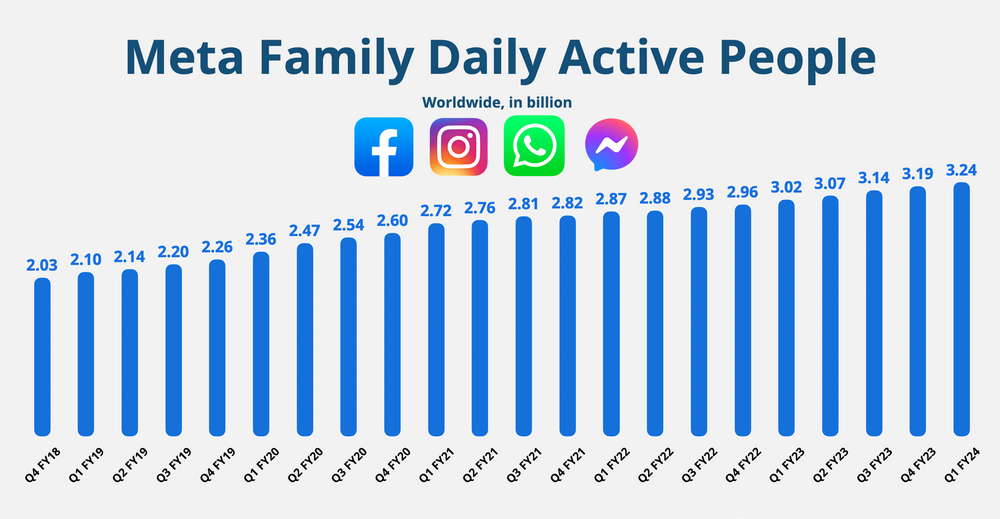

FoA's number of daily active people grew 7% year-on-year to 3.24 billion.

Zuck noted healthy growth in the US, especially at WhatsApp.

As expected, management stopped reporting individual Facebook metrics.

- Ad impressions grew +20% year over year (compared to +21% year over year in the fourth quarter).

- The average price per ad increased by +6% y/y (vs. +2% y/y in the fourth quarter).

Growth was strongest in Asia-Pacific and the rest of the world.

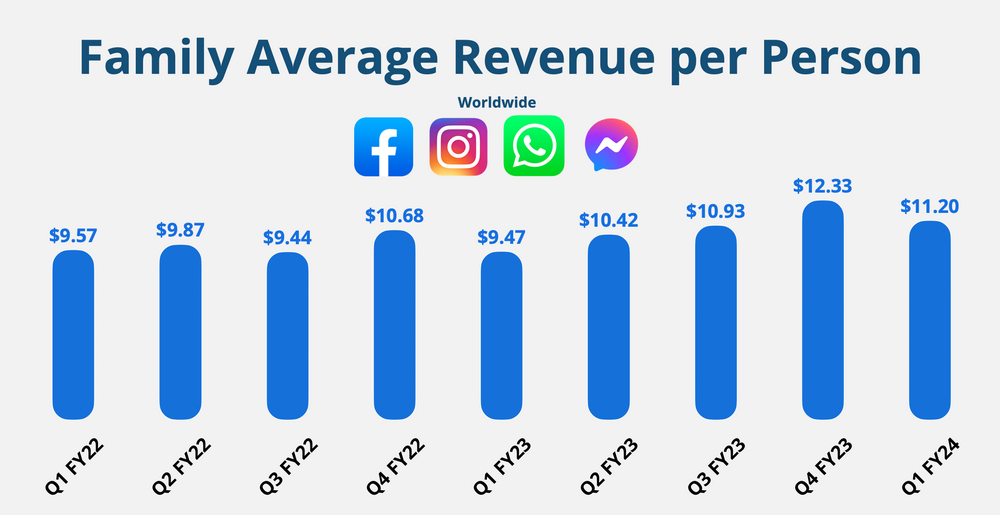

Average income per person increased +18% year over year to $11.20.

Higher engagement levels corresponded with continued strong advertising demand. By comparison, Snap's ARPU rose 10% year over year to $2.83 during the same quarter.

Note. Management has redefined ARPP and restated prior periods.

Certificate of income

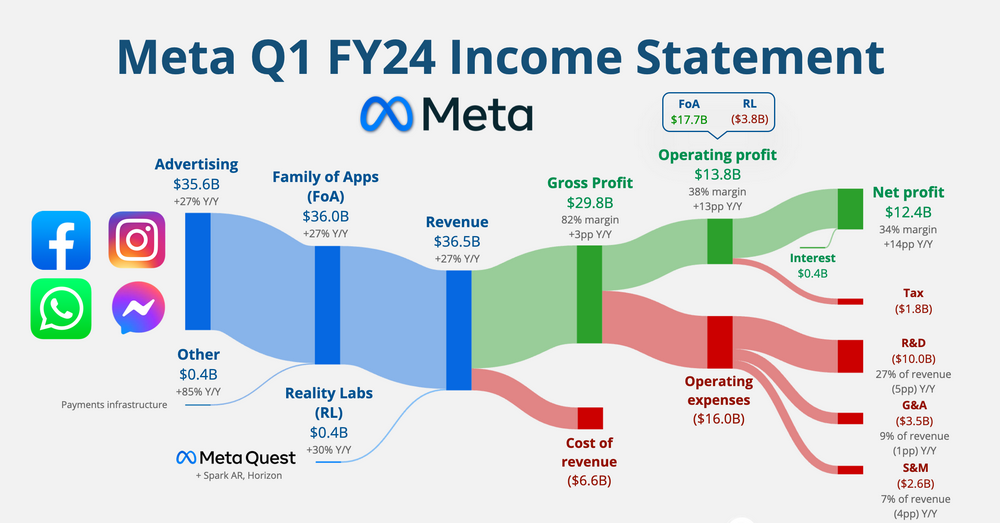

- Revenue grew +27% year over year to $36.5 billion (up $0.2 billion).

- FoA grew +27% YoY to $36.0 billion.

- RL grew 30% YoY to $0.4 billion.

- Gross profit amounted to 82% (+3 pp YoY, +1 pp QoQ).

- Operating margin amounted to 38% (+13pp y/y, -3pp q/q).

- FoA's operating profit amounted to $17.7 billion (profit margin 49%, +9 pp YoY).

- RL's operating loss was $3.8 billion, improving from $4.6 billion in the fourth quarter.

- Earnings per share rose 114% year over year to $4.71, up $0.39.

Cash flow:

- Operating cash flow amounted to $19.2 billion (profit margin 53%, +4pp y/y).

- Free cash flow amounted to $12.5 billion (margin 34%, +10pp YoY).

Balance:

- Cash, cash equivalents and marketable securities: $71.5 billion.

- Long-term debt: $18.4 billion.

Management:

- Revenue for the second quarter of FY24 was $37.7 billion in the midrange (expectation of $38.3 billion).

- FY24 spending is $96-99 billion (previously $94-99 billion).

- FY24 capital expenditures are $35-40 billion (previously $30-37 billion).

So what to do with all this?

- The increase in network users was consistent with the fourth quarter. Meta still found a way to add another 50 million users to its family of apps. However, it was a slight slowdown after four straight quarters of accelerating growth.

- Revenue grew +27% year over year in constant currency. This was another acceleration from +23% YoY in the fourth quarter.

- Advertising revenue growth was driven by: The online commerce vertical contributed the most to year-on-year growth, followed by gaming, entertainment and media. Growth was strongest in the rest of the world (40%) and Europe (33%).

- Reality Labs' revenue grew 30% on Quest 3. The smaller loss in this segment was primarily due to favorable restructuring cost competition last year.

- The number of employees increased sequentially by 3% to 69,300 people.

- Operating margins improved after a "year of performance." In FY23, Meta incurred $3.5 billion in restructuring charges (primarily business consolidation costs and employee severance costs). However, it consistently decreased slightly.

- Returning cash to shareholders. Share buybacks totaled $15 billion in the first quarter, a huge increase from $9 billion in the prior year. Management continues to view the stock as quite attractive. They also paid out $1.3 billion in dividends.

- Free cash flow hit a record in the first quarter, another highlight of the year's performance. Although Meta loses nearly $16 billion annually on Reality Labs, the company remains a cash printing machine ($48 billion in free cash flow over the last 12 months).

- The fiscal 2Q24 earnings outlook assumes a slowdown in growth. The average forecast calls for 18% year-over-year growth, which is likely the main reason for the negative share price reaction. CFO Susan Lee cited increasingly challenging conditions as Chinese advertisers recover in 2023.

- Capex and operating expenses for FY24 were increased primarily due to increased infrastructure investments to support the AI roadmap.

2. Latest developments in business.

🥽Horizon OS

Meta announced an open model of its Horizon OS, which runs its virtual reality headsets. They partner with hardware manufacturers like Lenovo and XBOX to develop headsets optimized for different use cases.

Why is it important

🔍Market Definition: Meta's real competition is not other VR headsets, but everything that competes for consumers' time and attention, including social networks, streaming services and games.

🧠Artificial Intelligence Lessons: With its open-source artificial intelligence model Llama, Meta realized that a company doesn't have to have the best models, but it does need a lot of them. The potential for content creation benefits Meta platforms, even if the models are not exclusively owned by them.

Main motivation

Zuck explained during the call: “There will be demand for more projects than we can build. […] Opening up our ecosystem and opening up our operating system will help grow the ecosystem even faster.”

🤖 Echoes of Android: Like Google with Android, Meta aims to create a platform that is not dependent on the Apple or Google ecosystems. This is a defensive strategy to protect their advertising business. The move to new vision-based computing experiences provides an opportunity to do just that.

Not Apple's model: Apple's highly profitable closed model is not ideal for Meta. They want to maximize reach, just like Android did. An open approach is natural.

Horizon OS Strategy

🥽Licensing model. Partnering with hardware manufacturers aims to expand the platform's reach and develop headsets for specific use cases that Meta couldn't do on its own.

🧑💻Developer Focus : Meta has an advantage in the VR developer community compared to Apple. A more open application model could reinforce this advantage.

🤖Meta AI

Meta AI is an intelligent assistant capable of complex reasoning, following instructions, visualizing ideas and solving subtle problems. It now runs on Meta's newest LLM family, Llama 3.

Llama 3 has two models: 8B and 70B, which have 8 billion and 70 billion parameters respectively. Currently, another model with parameters 400+B is being trained.

By now, Meta has a clear action plan for creating new products:

- Release an early version to a limited audience.

- Collect feedback and start improving it.

- Make it available to more people.

- Scale and refine.

- Monetize.

When more than 3 billion people use your apps, your ability to test and iterate is endless. The early release of Meta AI took place in the fall of 2023. They are now moving to the next phase by releasing the product in more countries through WhatsApp, Messenger, Instagram and Facebook.

During the Q&A session, Zuck talked about future monetization potential: “I do think that over time it will be possible to put advertising and paid content in Meta AI interactions, and also people will be able to pay for larger models or more computing resources, or for some premium features and such, but it's still very early days.

The biggest opportunity is certainly in business messaging and AI agents. “What the agent is going to do is you give it an intent or a goal, then it turns on and probably actually does a lot of queries on its own in the background to help achieve your goal, whether it's researching something on the Internet or ultimately you you will find the thing you want to buy.”

Beyond simple customer support, Zuck sees huge opportunity in deeper engagement with models to achieve business goals like retention and conversion.

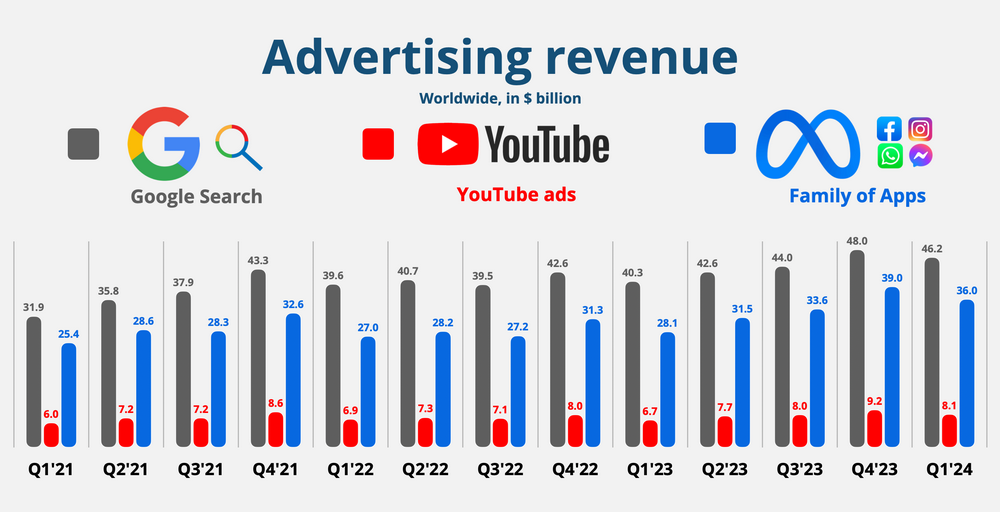

📊Market

Share Meta's ad revenue reached $36 billion in the first quarter, accounting for 78% of Google search revenue (+8 p.p. compared to last year). We'll have to go back to the second quarter of FY21 to find the two giants that close. The gap could narrow further later this year.

We'll take a look at Amazon's ad revenue in the coming weeks.

👨🏼⚖️Bill on TikTok

- Sell or trade: A bill to force the sale of TikTok (or ban it outright) was signed into law this week. This is due to national security concerns about the possibility of misuse of data and propaganda by the Chinese-owned app. The company has nine months to find a buyer.

- Legal challenges ahead: TikTok will likely challenge the law in court, citing First Amendment rights (free speech).

- Not so fast: even if he is forced to sell, it will be difficult to find a buyer:

- 🏷️ Price tag: Wedbush estimates TikTok's value in the US at $100 billion.

- 🔍 Verification: The US government must approve any buyer.

- Policy: China may block the sale to maintain control.

- Who would buy this? Potential buyers are in rarefied air. Microsoft, Oracle, Walmart and Amazon are often mentioned. But this is all speculative.

- Indiscriminate asset sales: The real value lies not only in TikTok's audience size, but also in its recommendation algorithm. Spinning TikTok from Chinese parent company ByteDance could be challenging due to technology and a global workforce.

- Long term: A forced sale can significantly change the appeal and value of an app. A TikTok app without its algorithm could become less attractive, which would ultimately benefit any company competing for our attention, including Meta.

3. Key Quotes from the Income Statement

Founding CEO Mark Zuckerberg

On AI in Meta Products:

“We're building a range of different AI services, from Meta AI, our AI assistant that you can ask anything you want in our apps and glasses, to Creator AI, which helps creators engage their communities and that fans can interact with, to business -AI. which we think all the companies on our platform will eventually use to help customers buy things and get customer support, for internal coding and AI development, for hardware like glasses, for human interaction with AI, and more another."

He also shared some interesting points:

- Approximately 30% of Facebook posts are recommended by AI.

- More than 50% of Instagram content is recommended by artificial intelligence.

About investing in AI:

“We have the talent, data and ability to scale infrastructure to build world-leading AI models and services. And this leads me to believe that in the coming years we should invest significantly more in creating even better models and the world's largest artificial intelligence services. As we scale capex and opex on AI.”

He added that earnings will lag behind investments in artificial intelligence, reminding investors to be patient. The scaling phase will precede the monetization phase. Meta's track record of monetizing new products, most recently with Reels, is proof of this. Meta is well positioned to develop profitable artificial intelligence through greater involvement in its applications.

Regarding the FoA vs RL report:

“Increasingly, the work of our reality labs is aimed at supporting our efforts in the field of artificial intelligence. We currently report our financial performance as if Family of Apps and Reality Labs were two completely different businesses, but strategically I view them as fundamentally the same business with Reality Labs' vision to create the next generation of computing platforms, largely degrees so that how we can build better apps and experiences around them. Over time, we will need to find better ways to articulate the value created here in both segments so that it doesn't feel like our hardware costs are increasing as we scale our eyewear ecosystem, and all the value is flowing into the other segment.”

Looking at Meta's operating margins as a whole is probably the best way to evaluate the effectiveness of its strategy (rather than focusing solely on RL losses).

About AI agents:

“We've been testing the ability for businesses to customize AI for business messaging that introduces them to customer chats, starting with supporting shopping use cases such as responding to people asking for more information about a product or its availability.”

This initiative is still very early, but it could become a significant business in its own right.

In topics:

“There are now over 150 million monthly active users worldwide , and overall they continue to be on the trajectory that I was hoping to see.”

This is up from 130 million last quarter. While using monthly active users (instead of daily) may increase perceptions of engagement, the number is impressive for an app that's only 10 months old. Contrary to the predictions of most skeptics, the app is thriving despite the initial hype.

Chief Financial Officer Susan Lee:

About video content:

“ Video also continues to grow on our platform and now takes up over 60% of time on both Facebook and Instagram. Reels remains the primary driver of this growth, and we continue to work to bring Reels, long-form video and live video together into one seamless experience on Facebook.”

60% is another significant increase in video content, previously “more than half.”

About advertising and interaction:

“We are getting better at adjusting ad placement and quantity in real time based on our perception of user interest in ad content and minimizing ad clutter, and innovating in new and creative ad formats. We expect to continue this work going forward, while relatively lower monetization areas such as video and messaging will provide additional growth opportunities.”

In addition, new advertising models provide greater efficiency for advertisers, such as Meta Lattice, a new ad ranking architecture that can run larger models that generalize learnings across different surfaces.

4. What should investors and traders watch out for?

Here's the first quarter news on what I'm keeping a close eye on:

- 👨👩👧👦 User growth. The family of applications added about 50 million daily users. How long can this impulse continue?

- 🧵 Topics: 150 million monthly active users 10 months after launch allowed the app to become a mainstream platform over time. But don't expect monetization in FY24.

- 🔓 Lllama 3: The latest open source version of LLM sets a new standard. The even larger 400B parameter model currently in development could be a game-changer and a big step forward in the field of generative artificial intelligence.

- 🤖Meta-AI: It’s critical to keep an eye on new use case announcements, especially for business messaging.

- 🛍️Advantage+ and In-Store Advertising: Meta's latest updates offer AI-powered tools that automate creative content, personalize ads, and showcase detailed product information in more engaging ways. Store advertising revenue reached $2 billion in FY23.

- ⚖️Regulators: In addition to the TikTok drama, Meta has a jury trial in Texas over the use of facial recognition. There are always new investigations approaching that could potentially challenge the status quo.