")

")

")

")

")

")

")

")

")

")

")

")

")

")

The largest US banks by capitalization

During the period of US bank reports, the Masters will show you the macroeconomic indicators of the largest US banks.

JPMorgan CEO Jamie Dimon said: “Many economic indicators continue to be favorable. However, as we look to the future, we remain vigilant to a number of significant uncertain forces.”

Recall that banks make money through two main income streams:

Net Interest Income (NII): The difference between interest earned on loans (such as mortgages) and interest paid to savers (such as savings accounts). This is the main source of income for many banks and depends on interest rates.

Non-interest income: income from services that do not involve interest. It includes commissions (such as ATM fees), advisory services and trading income. Banks that rely more on non-interest income are less exposed to changes in interest rates.

Here are the key developments in the first quarter of FY24:

NII's outlook is changing: While net interest income delivered strong earnings in 2023, first-quarter earnings signaled a slowdown in growth. Banks were forecasting a decline in NPV or more modest growth as the rate hike cycle potentially ends.

Mixed results: Investment banking saw a revival for some banks, such as Bank of America and Goldman Sachs, while others showed continued weakness compared to the 2021-2022 boom.

Focus on asset management: This area has seen steady growth at banks such as Morgan Stanley, Schwab and Goldman Sachs, highlighting the growing importance of fee-based income streams.

Consumer Lending Alert: Some banks are increasing provisions for loan losses, especially on credit cards and wholesale loans, signaling a more cautious approach to consumer lending.

Strategic Transformation: Ongoing restructuring initiatives are a common theme. Banks such as Citigroup and Wells Fargo are focused on streamlining operations and exiting less profitable businesses to achieve long-term efficiency.

Regulatory Challenges: Banks continue to address challenges raised by past regulatory scrutiny by making ongoing remediation efforts and adapting to changing risk management requirements.

Impact of FDIC Assessment: The Federal Deposit Insurance Corporation (FDIC) imposed a fee on banks with more than $5 billion in assets following the collapse of Silicon Valley Bank and Signature Bank. They will collect fees for eight quarters starting in the first quarter of 2024, creating a near-term headwind to earnings.

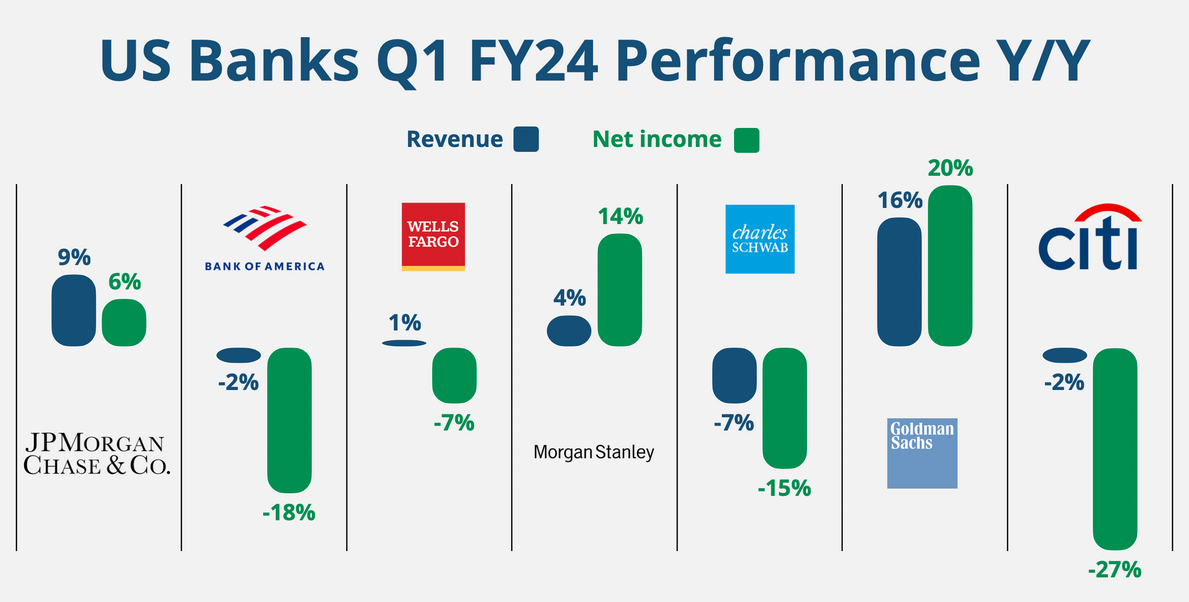

Here's a quick look at Q1 FY2024 performance compared to last year.