")

")

")

")

")

")

")

")

")

")

")

")

")

")

Early elections in France, bets in the USA, problems in the Chinese auto industry, artificial intelligence and company news

• Investors in Europe will start the week with uncertainty about the outlook for global interest rates and the political landscape in the region.

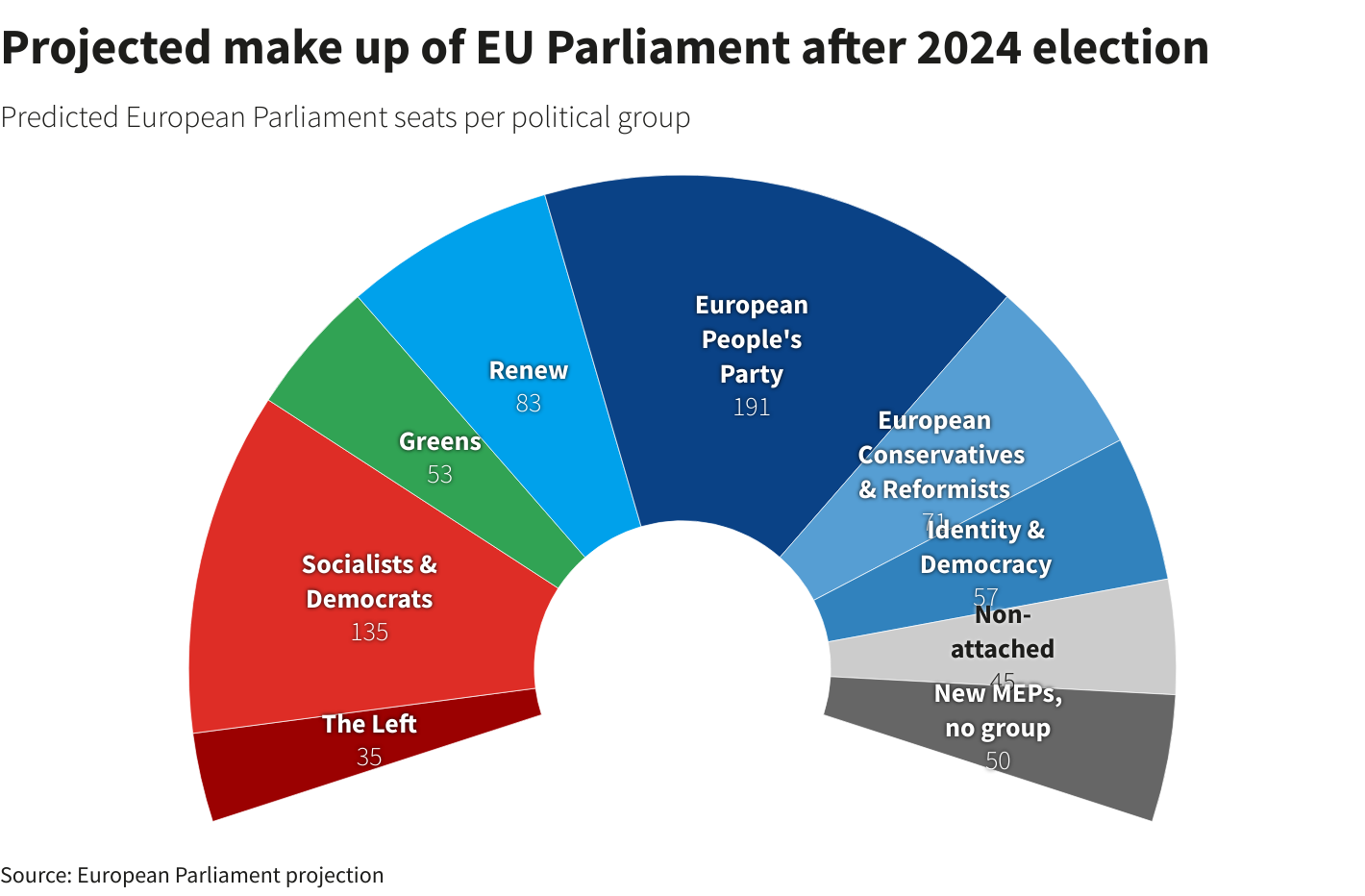

• French President Emmanuel Macron has called early legislative elections later this month after he was defeated in European Union elections by Marine Le Pen's far-right party. His shock announcement came as the European Parliament shifted to the right after four days of elections that ended on Sunday, with more Eurosceptic nationalists and fewer mainstream liberals and greens. Marine Le Pen's far-right National Rally party won the European Parliament elections in France " She was more than twice ahead of Macron's Renaissance party - 31.5% versus 15.2%, respectively. Macron dissolved the National Assembly and announced early elections to the French parliament for June 30 and July 7 (first and second round).

• In the broader market, traders also continue to weather the fallout from a sharp US jobs report ahead of the Federal Reserve's June policy meeting this week. The rate-cut rally that sent global shares higher last week quickly stalled, leaving Asian shares in a tight spot on Monday, although trading was slowed by holidays in Australia, China, Hong Kong and Taiwan.

• Traders have also lowered their expectations for a Fed rate cut - the likelihood of a pre-election rate cut is now less than 50-50, and two full rate cuts are no longer in the cards for this year. Fed policymakers will abandon their forecasts for three rate cuts this year, they will announce their rate decision on Wednesday, it's almost a given that the question is by how much. Futures indicate about 36 basis points of rate easing are on target this year, and the chances of a pre-election rate cut remain a coin toss.

• In addition to the Fed, the Bank of Japan will also meet this week and the central bank is expected to announce a reduction in its large bond purchases. That could provide some respite for the yen, which was still struggling above 157 per dollar against the recovering greenback on Monday.

• On China, U.S. officials expect G-7 countries to issue a stern new warning to smaller Chinese banks at a summit this week in Italy to stop helping Russia evade Western sanctions, according to two people familiar with the matter.

• Volvo is considering moving the production of some cars from China to Belgium. The Swedish-headquartered company is majority owned by Chinese automaker Geely, in anticipation of the European Union cracking down on Beijing-subsidized imports. And on Saturday, Turkey said it would impose an additional 40% tariff on car imports from China.

• Miners sell electricity to AI for $3.5 billion. Mining company Core Scientific will rent out 200 MW of power for 12 years in its own data center for training artificial intelligence models. This will bring the company about $300 million a year (more than $3.5 billion over 12 years) and will partially cover the decline in its income after the Bitcoin halving.

• Within five years, will everyone have their own AI assistant? These forecasts were shared by DeepMind co-founder Mustafa Suleiman. And it's not just about performing automated tasks. Everything will go further: artificial intelligence can become a full-fledged human assistant - a coach, advisor and even life partner.

• For diamonds, it is important who De Beers will cooperate with next - WSJ. Because more and more American couples are choosing lab-grown stones. So those buying shares in the world's most famous diamond manufacturer need to be careful.

• Elon Musk said a key group of Tesla shareholders supported his large compensation package - Barron's.

• The world's biggest economies are seeking to halt new private sector coal financing - Reuters. Some of the world's largest economies want to finalize a plan before the UN climate change summit COP29 this November to stop new private sector funding for coal projects

• Ford CEO for Barron's. The growth of electric vehicles is fading, forcing the wider industry to question whether it is spending billions of dollars wisely. Politics, car availability and charging infrastructure are all to blame.

- The main events of this week will be the May inflation data and the Fed's interest rate decision

. - On Wednesday morning, the Bureau of Labor Statistics will present the consumer price index for May.

- The Fed will announce its decision on Wednesday. No changes are expected.

- The BLS will release the May Producer Price Index on Thursday.

- On Friday, the Bank of Japan will publish its decision on monetary policy.

The major corporate events on the earnings calendar this week will be

Oracle on Tuesday, Broadcom on Wednesday and Adobe on Thursday.

Today

- FDA Decision Dates for Genfit Elafibranor (GNFT), Amgen Tarlatamab (AMGN), and Bristol Myers Squibb Repotrectinib (BMY).

- Apple WWDC conference. The key topic of the event will be generative AI. A potential announcement of a collaboration with OpenAI could give investors insight into Apple's AI strategy.

- Amazon (AMZN) will host a three-day AWS re:Inforce conference. The focus will be on data protection, threat detection and incident response, network and infrastructure security, generative AI, and application security.